“Do not be impatient with your seemingly slow progress. Do not try to run faster than you presently can. If you are studying, reflecting and trying, you are making progress whether you are aware of it or not. A traveler walking the road in the darkness of night is still going forward. Someday, some way, everything will break open, like the natural unfolding of a rosebud.” –Vernon Howard

This quote applies to the cashflow journey beautifully:

If you don’t have any money to invest, or just don’t know where to start, don’t fret grasshopper. Network and read. Talk to whomever you can. Look for local investor meetup groups. Never stop learning, always keep an open mind. Read a book (I like Rich Dad, Poor Dad). Read a blog (I like MMM or Bigger Pockets). Ask questions of anyone (people who’ve achieved what you’d like to achieve are highly preferred over friends/family). Knowledge is power. This is a journey, not a race.

DISCUSSION OF RECENT CHANGES:

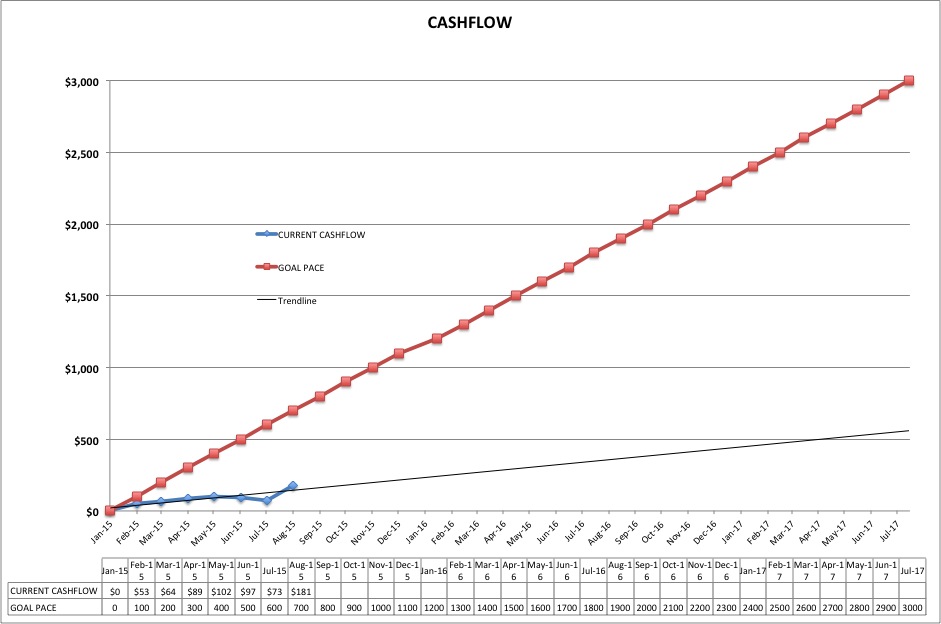

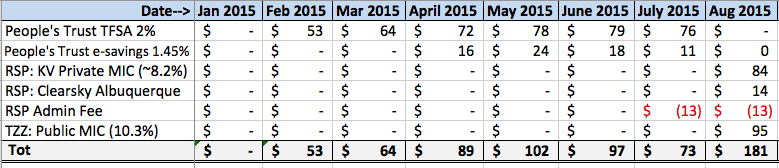

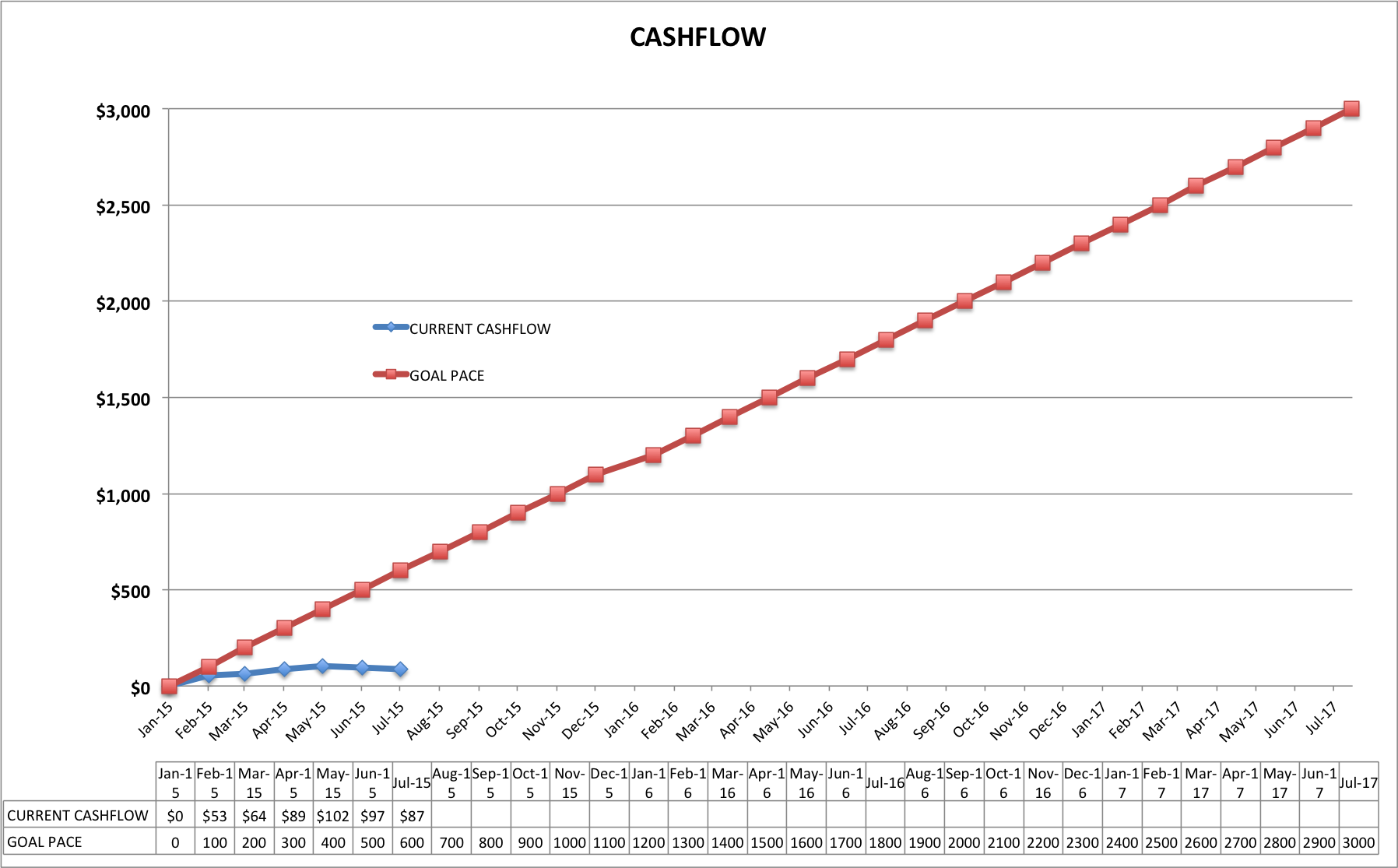

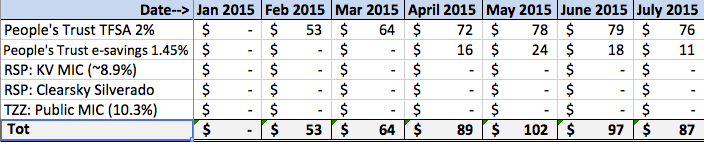

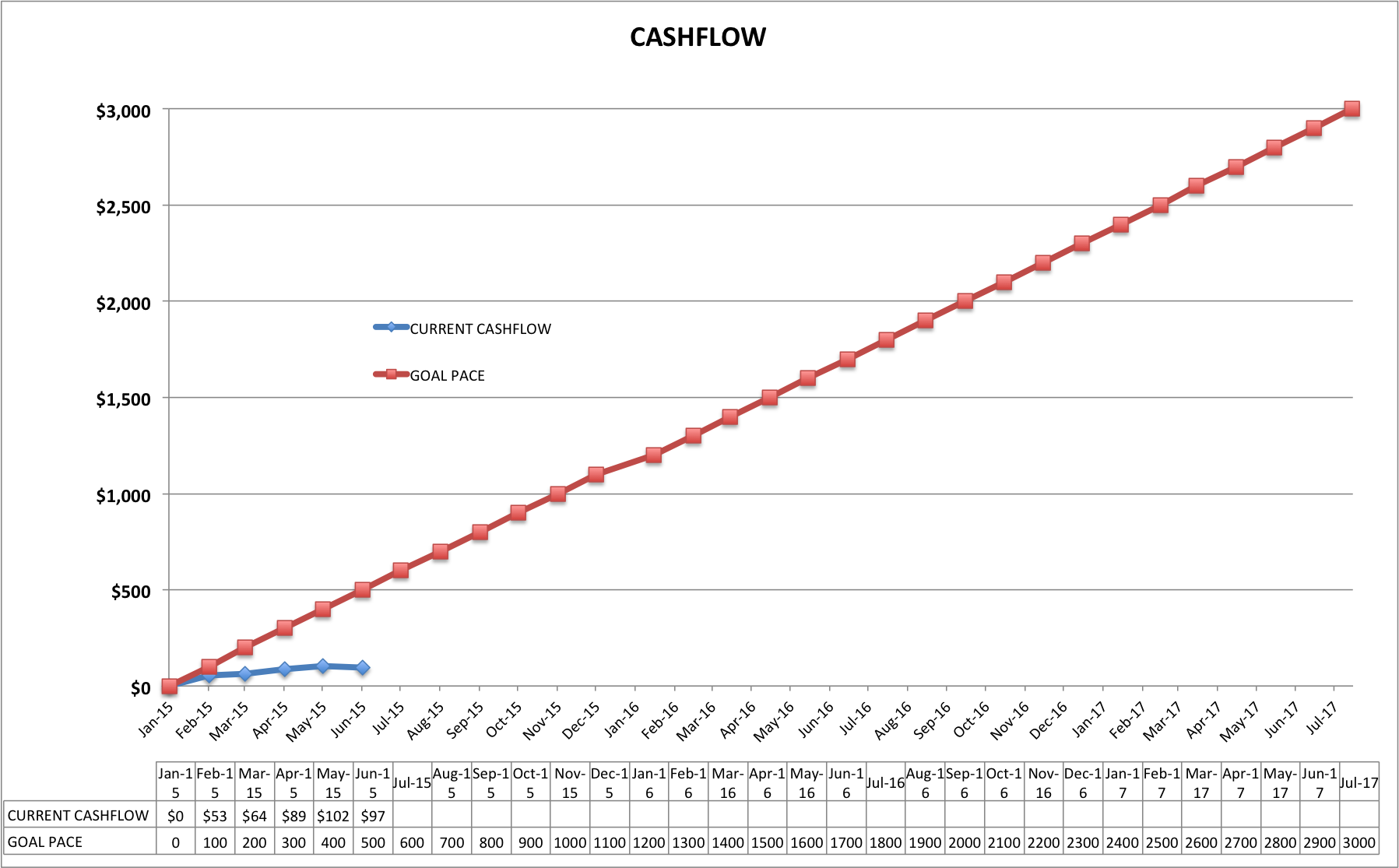

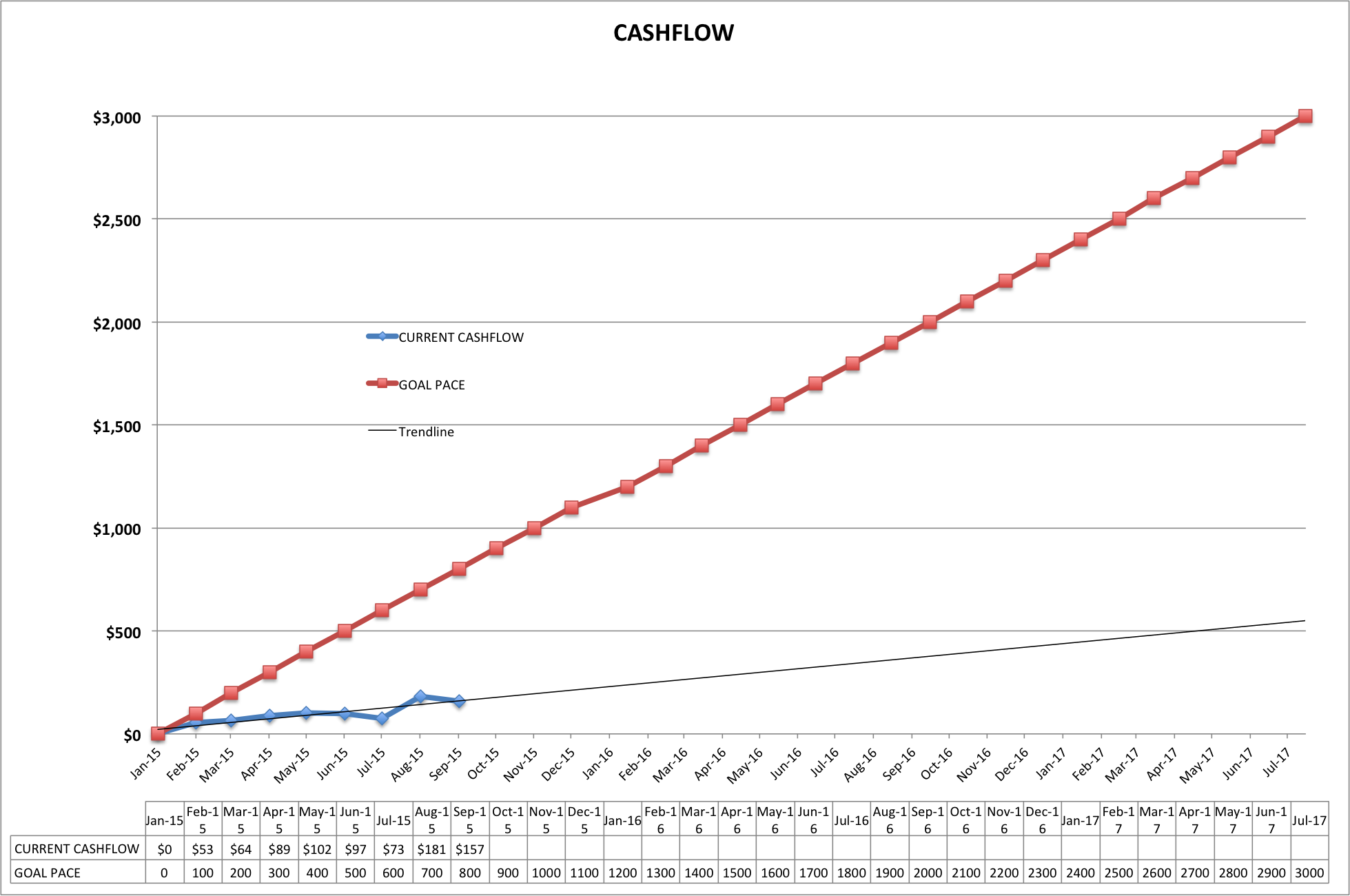

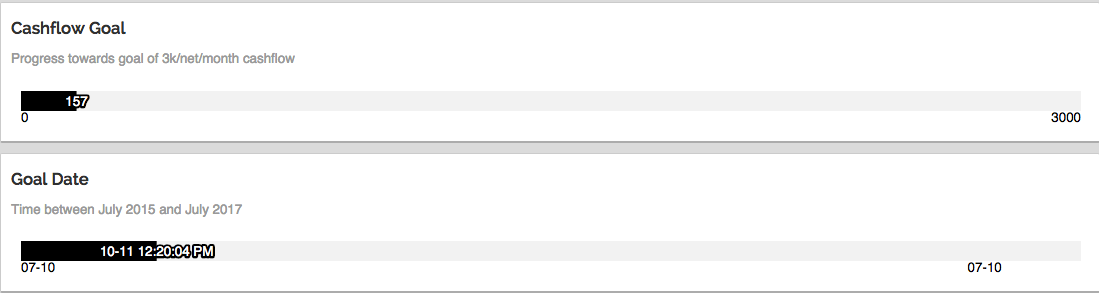

The graph now more accurately reflects cashflow with the retroactive addition of an RSP fee.

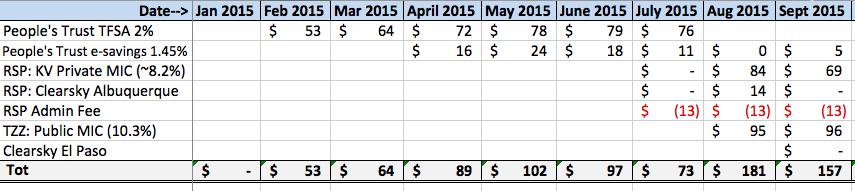

I invested in another Clearsky US Real Estate offering (an apartment in El Paso). The selling feature for me was that this deal is more cashflow oriented (6-8% target). However, the downside again is that my money is locked in for the life of the deal (4-7 year target) so that is the tradeoff.

I also closed out my position in TZZ (public MIC), for a miniscule overall gain. The volatility made me super uncomfortable. From late July until today, it had a range of 5.71 – 6.88. This represented swings of over 10% more than once. Yikes! Protecting capital is the #1 rule before seeking higher returns.

Q & A SECTION?! Whee!

Let’s do something fun. I thought I’d share one of my friends’ comments (totally paraphrased of course), in case there’s some parallels with you. *Please keep in mind I’m NOT a financial planner, nor do I play one on the interwebs, so please take everything I say with caution, as I’ve given bad advice in the past.

A reader writes: “Hey man, long time reader, first time writer. I’m inspired to do something similar! Maybe I should keep track of my finances too. However, I don’t really know anything about money management. But I do have a small savings account sitting there…. etc. xoxo”

Here’s what I’d recommend: open a People’s Trust e-savings account. With this you’ll earn 1.45% (as of today’s writing. It could change at any time). Or perhaps their TFSA savings account (2%) might be a better fit for you? (Don’t forget to familiarize yourself with the TFSA rules!)

Why?

- Liquidity. Once you have it set up and linked to your daily bank account, I find it takes about 3 days to deposit/withdraw money, via online banking. This keeps your options open, it’s not ‘locked-in’. Maybe you want to save for a down payment on a home, find an investment, or you have no f-ing clue yet. This is a great ‘temporary placeholder’ while you figure that out.

- Habits and mindset. Once you start to make money each month for doing nothing**, you start to think, hm, maybe I should do more of this. It starts that ol noggin thinking about it. And at least you can feel good about doing something instead of nothing with your cash.

- Baby Steps. What can be simpler than a free high interest savings account? (Hint: nothing). Everyone can understand it. Don’t run before you can walk. Park your savings here while you take your time to learn about options and vehicles that might best suit you.

I would also add: read Rich Dad, Poor Dad. Seriously. I know several people whom this book has changed the course of their life, and that’s no exaggeration. Hop on a bike and head down to your local library where you can borrow it for free 🙂

Cheers and happy cashflowing!

*Giving advice to friends is something I’m really afraid of nowadays. In 2007 I invested in mutual funds, was super stoked about it and remember talking the ear off a good friend about it. We all know what happened to stocks a year later! From 2008-2014 I was really into precious metals investing, and remember talking to friends about them with similar enthusiasm. They did quite well until 2011-2012ish, but shat the bed hard in 2013. It’s very possible some of my good friends got burned because of choices I may have influenced. So this is why I now prefer to simply share what I’m doing with my savings, but don’t really like to recommend anything. Except for People’s Trust haha, they should be super safe 😉

**Of course we know that’s actually not true! You will have spent time doing research, setting up accounts, not to mention working fucking hard to earn and save that durn money in the first place!