“In school, the person who makes the fewest mistakes wins. In life, the person who makes the most mistakes wins.” –Robert Kiyosaki

Hey guys!

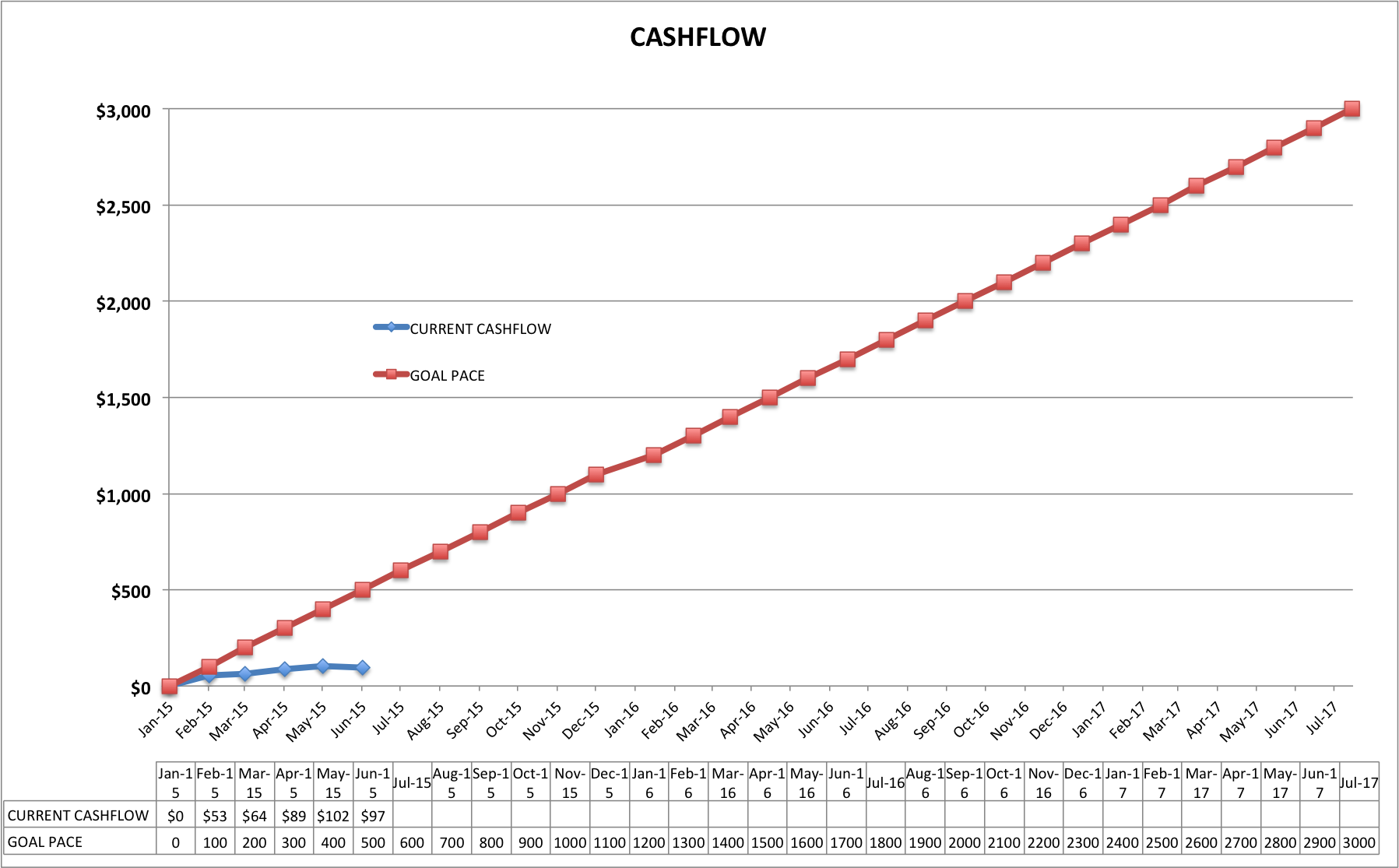

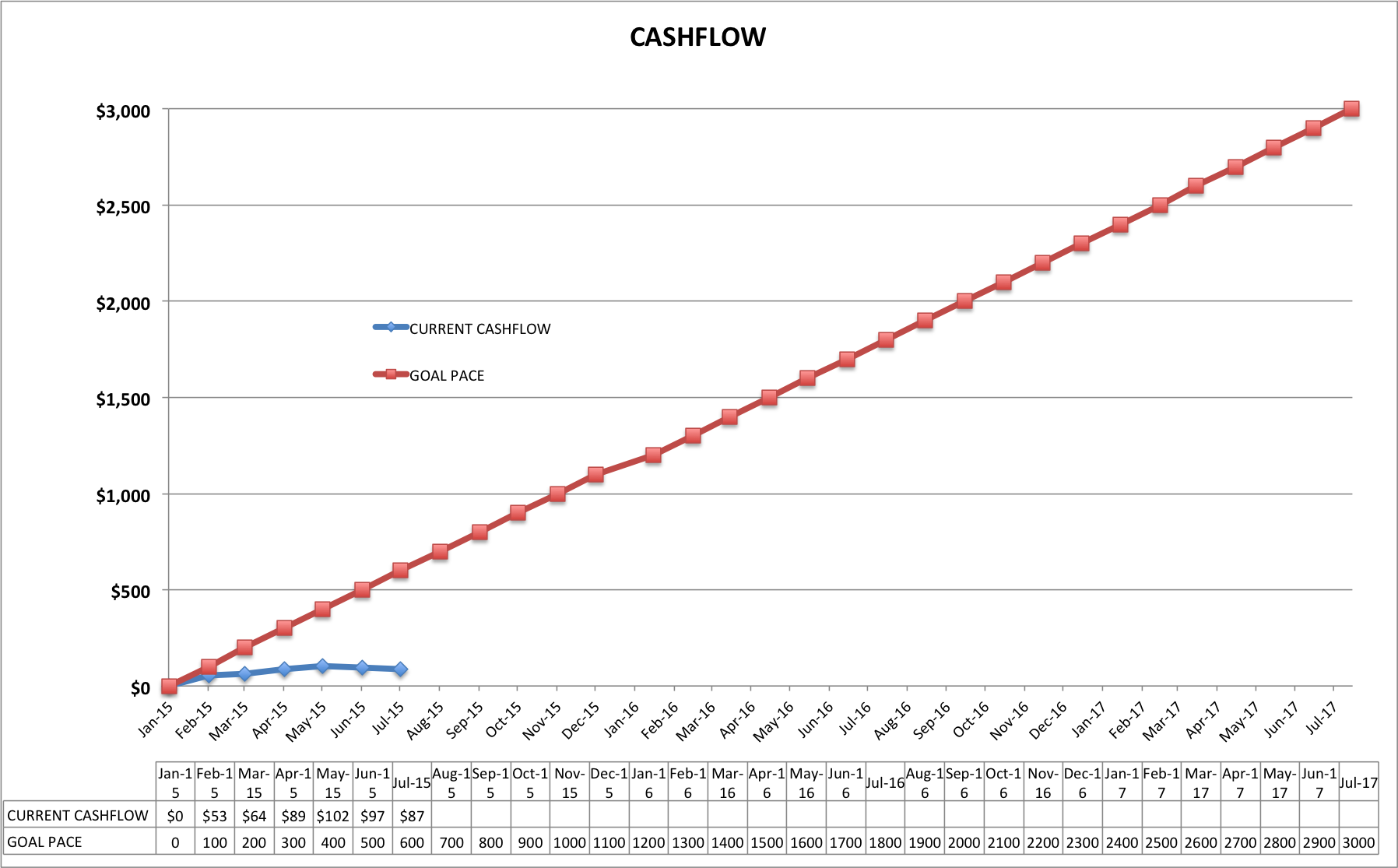

Once again, July’s update is super boring. I had hoped to see the fruits of recent changes, but they have yet to take effect. For now, I’m embracing what they call the ‘J-curve’: lower cashflow now, while I optimize, experiment and tweak things. It’s boring, but it’s all about being transparent and sharing the journey. And for now, the journey is anything but glamorous.

Let’s discuss what’s new:

(**Update Sept 2015: Please see discussion of MIC’s in Aug 2015 Update. I no longer recommend investing in any publicly traded MIC!).

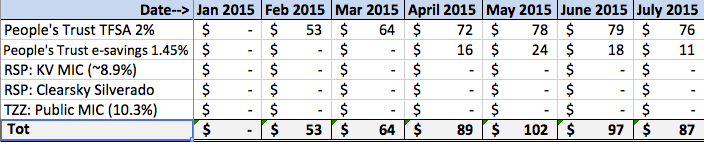

Holy crap! A stock that pays >10% dividends on a monthly basis? Yes. I shuffled money out of the e-savings 1.6% and into this. If you hold stock on the third to last business day of each month, you get paid dividends around mid-month the following month. They also offer a DRIP program. My purchase price was $6.82/share and monthly dividends are currently $0.0583/share for a 10.3% annualized return. It seems too good to be true and alas might be: in their latest financials, due to loan defaults, they mentioned a possible dividend reduction in October, and the stock performed accordingly. It’s possible the dividends might be reduced to around $0.046/share/month, or ~ 8% annualized return based on my purchase price of $6.82. This seems to be typical of the luck I tend to have: they have steady dividends for 3 years and the moment I buy it could be reduced by 20%. Gah! I can’t tell you how many times similar things have happened to me lol :S

Other point to note is that People’s Trust has continued to reduce their interest rates: what was once a 3% TFSA when I signed up in Jan is now 2%, and the e-savings has gone from 1.8% to 1.45% (Do you see the pattern emerging with my timing here?). This is in step with several government policies (more TFSA contribution room, lower Bank of Canada interest rates) and certainly makes them less attractive products, but still a good ‘placeholder’ option.

Ok that’s it for news! So we’ve already gone from 1.8% and 2.25% vehicles a few months ago, to finding over 10% returns, all as monthly cashflow. BUT it doesn’t take a rocket surgeon to figure out even compounded 10% returns won’t get me close to my goal in 2 years. Maybe in 10 years with super-frugal savings, yes. But continuing to live the kind of frugal lifestyle I’ve been for the past 3 years, as well as working the jobs and schedules I’ve had during this time, for the next 10 years, simply isn’t acceptable. It’s going to take much more creative, bold strategies.

ENTER REAL ESTATE INVESTING

The only vehicle I’ve been able to find that could achieve my goal in 2 years is real estate. Within real estate there are myriad approaches, niches and variables. Over the past several months, I’ve finally defined a clear goal (3k net permanent monthly cashflow by July 2017 starting with 75k capital) and have been examining different REI (Real Estate Investing) strategies that might achieve this. I networked with real estate agents, lenders and local investors, toured homes for sale, emailed lots of people, talked to friends also into REI, etc. (By the way, if you or anyone you know is into REI, let me know! Networking has been the single biggest tool and help so far, and you never know what you might learn. I’ve met some amazing contacts that either are, or might one day be, part of my ‘team’). A common theme has been that potential cashflow is higher in the US than Canada, due to the housing crash we didn’t have. Furthermore, prices are lower in certain markets, affording someone with limited capital a lower point of entry. A great resource has been Bigger Pockets. One strategy I looked at really closely was applying the BRRR method, both in Victoria and Nanaimo. Unfortunately, several pieces were still missing (capital & financing/refinancing chief amongst them) for these to be a really good fit locally. It was more realistic in Nanaimo than Victoria, but again, the pieces and fit wasn’t quite right.

So I’ve recently decided to turn my energies southwards, for the time being. With my summer job not panning out, the timing is ripe. I’m excited to see what happens over the coming months, and will report here as things actually unfold (but not before hand as I don’t like speculating). I’m taking a risk, I’m scared as hell, but it’s what I have to do to achieve my goals and dreams, and hopefully we’ll have some exciting progress and things to talk about on here soon!

Stay tuned and happy cashflowing!