“An expert is a person who has made all the mistakes that can be made in a very narrow field.” – Niels Bohr, Danish physicist and Nobel prize winner.

I like quotes like this – they make me feel better about myself. In keeping with this theme, we’ll discuss some recent mistakes I’ve made in my cashflow quest. My hope by sharing is you can learn and benefit from them 🙂 But first, as always, the graphs!

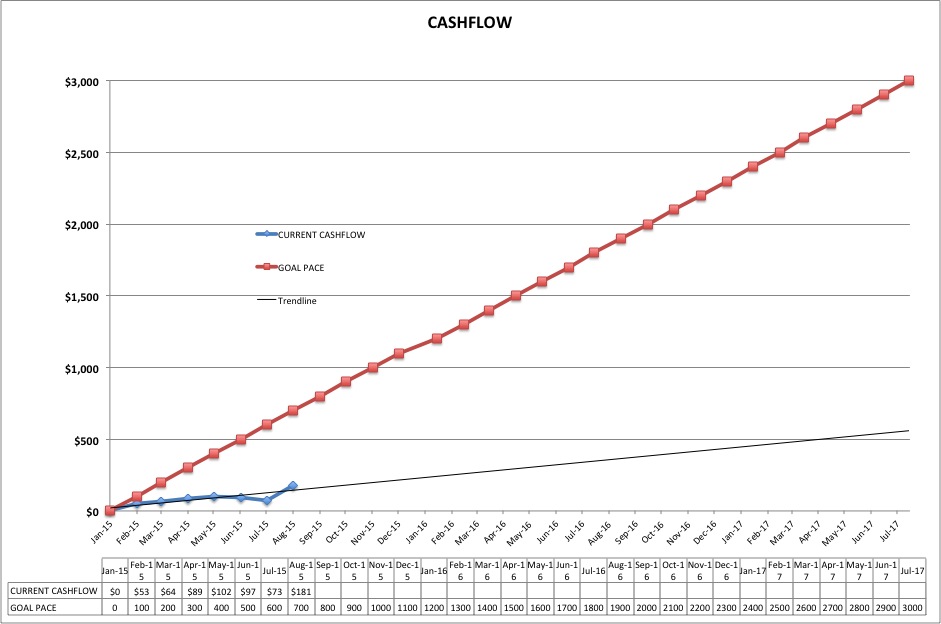

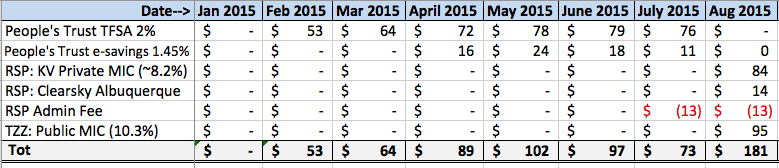

Okay! It looks like the J-Curve has started picking up with the changes initiated in June finally kicking in. I wish these things were instant, but that’s life. Building passive income is slow at first until it will snowball. And it will. Also, we’re now at nearly $200/month which is slightly notable, but not enough to be exciting yet. We are laying the foundation.

More MIC crap again?!

I want to revisit MIC’s briefly. I can hear you sigh. Sorry, but they’re a key part of my long-term strategy, so it’s important to get them right. I’ve quickly learnt the hard way that not all MICs are created equal. In the June post I raved about these and was stoked to have discovered high yielding publicly traded MIC’s on the TSX. I was stoked on their high returns and liquidity. I then invested in one (TZZ) and nearly in a few more (TMC, etc). Well this, as the opening quote suggests, was a mistake. I now regret this. Although the cashflow, paid in monthly dividends, is high at 10.3%, the volatility has been unreal, stupid and simply unacceptable for what should be a stable investment. I can’t stomac it, and I can eat a lot! Also, the track record of some of these publicly traded MIC’s in terms of stock price, is one of ever-decreasing valuation, even if the dividend remains unchanged or little changed. I should have known, I saw the historic charts, but I was blinded by the high returns. What good is a 10% dividend if you loose 10%+ of your capital (stock price valuation) per year? Exactly. No good is the answer.

On the other hand, I’m very pleased with KV so far. It’s pumping out just over 8% (*annualized), reinvested monthly. And my underlying capital doesn’t fluctuate wildly like the ones on the TSX. The trade-off is it’s less liquid in terms of getting in/out than the stocks (and there’s fees to getting out too. Graduated (decreasing) with the number of years since you got in). However, it’s in my RSP, so that’s OK. So if you are going to get into a private MIC, please consider the liquidity and how it matches your situation.

I emailed Gordon Johnson, the author of a good book I recently read called Turn Your Mortgage Into a Pension. I highly recommend this enlightening read about a powerful financial strategy tailored for Canadians.

I’ll just copy/paste his reply, as it says it all:

Hi Erich,

I would not invest in publicly traded MIC’s. The public market is volatile and share value often has no relation to underlying value.

Private MIC’s do not have the volatility of public MIC’s. Typically they have great track records and have proven themselves to be stable investments over time. The same is true of REIT’s. Public REIT’s can be volatile, whereas private REIT’s tend to be stable in their valuations and returns. Look at Centurion REIT compared to public REIT’s during the last downturn in the markets.

KV is a good MIC. I am also quite familiar with Antrim Investments and AP Capital (formerly Alta-Pacific). Antrim is the MIC I refer to in the table in my book. I chose Antrim as it is one of the largest and most conservative MIC’s in Canada. Both KV and AP have demonstrated better annual results than Antrim. Antrim is much larger and more conservative. Invests primarily in 1st mortgages. Liquid with no penalty. Pays quarterly dividend. Both KV and AP pay monthly.

REIT’s have a tax advantage over MIC’s in distributions. Typically the return is paid as return of capital which incurs no taxable income (0% tax). Capital gains in the future (taxed at 50% of gains). MIC’s income is fully taxable (100% of interest income is taxed, unless sheltered in an RRSP or TFSA).

None of the MIC’s or REIT’s mentioned above have lost 1 cent of investors capital – this is an important consideration for me when I look for an investment vehicle. I also want strong management and long history of returns (10 years if possible)…

So there you have it. Don’t invest in public MICs kids! To me this previously would’ve seemed counter-intuitive: old Erich thought private investments sounds secretive and sketchy, whilst public investments seem open and transparent and if so, the market should be efficient at valuing them. New Erich thinks “Aaaarg, fuck the stock market!!!” I need to research Antrim and AP now, perhaps they might offer the best combo of returns & liquidity I am seeking for my “placeholder” savings??

(**Update: AP Capital has similar graduated penalties as KV for getting out if held under 5 years, plus a $350 processing fee, and also even more restrictive liquidity: you can only cash out once a year. Being less liquid and paying slightly lower returns than KV means AP doesn’t interest me for now. Antrim doesn’t have fees for getting out, but it will likely take 2-3 months to get your money according to what I can tell from their OM, so let’s call it semi-liquid. (I spoke with their Director & Portfolio Manager on the phone and it sounded like they can often do it quicker, but they don’t like to. This investment is generally not for people who go in/out often or short term he said).

Tax strategies:

I’m slowly learning the value of a proper tax strategy. Again, based on mistakes about where I’ve “placed” my investments, which is currently not optimal. I’ll have to pay taxes on some of my cashflow, whereas if I had of structured things better I would not have had to pay taxes. Learn from my mistake kids! Here’s what I learnt today:

- Interest income: taxed 100% at your highest marginal tax rate (added on top of your income by the CRA). MIC dividends fall into this category.

- Capital Gains Income: taxed at 50%. Cashing out of a REIT or similar (eg. my Clearsky investment) falls into this category.

- Return of capital: taxed at 0%. Dividends/distributions from REITs/Clearsky, fall into this category.

In a nutshell, from a permanently-living-off-of-cashflow perspective (the goal, nay, the dream!), this means a MIC is better to place in your TFSA (0% tax). REITs, or similar investments such as my Clearsky investment, are generally better for cashflow outside of tax-sheltered vehicles: you get 0% tax on the monthly/quarterly distributions (treated as ‘Return of capital’), and are taxed on 50% of any gains only once you cash out.

You can also hold all these investments in a corporation, which would get taxed at the highest tax rate (~44-46%). However, my accountants feel that there is some kind of magic they can do to get this tax rate down to around 19-20%. So there is a lesson straight from Rich Dad, Poor Dad: surround yourself with a good team, accountants amongst them. (Also, shop around until you find a good accountant you’re satisfied with. It never hurts to get a second opinion. I recently networked with a local businessman & real estate investor who is onto his 4th property now. He said he’s on his 3rd accountant now, the current one being much better than the last, saving him thousands.)

US REI:

I wanted to talk about recent developments in pursuing real estate investing in the US, but this post is long enough. It’s a slow and arduous journey anyways, so you haven’t missed much. Till then, I really hope some of this has been useful and happy cashflowing you guys! Feel free to share your graphs and we can celebrate together!

Hi Erich

Thanks for the update. Great information here for the non-informed, mis-informed, ill-informed etc. Straight information is a welcome change to the investment scene.

John Watson

LikeLike